If you want to follow along with my own journey toward financial independence and early retirement, and to understand my thought process and the numbers behind it, this is the post for you.

One of the first posts I made on Retire29 was a roadmap laying out the details of my plan to go from a financial train wreck to financial independence. I called it, “The Big Goal Roadmap.”

As with any long journey, there will be detours, flat tires, and the whining kids in the back seat; these things that are unforeseen will impact the route and timeline. This is my first update to my big goal roadmap, and serves as the new Roadmap. My desire to reach financial independence and to exit the workforce is as strong as ever, however, the means to the end has somewhat changed, and I want to illustrate those changes with a fresh look.

So, a year after starting the journey, it is now time to reassess and see how things are going.

The Roadmap

Retirement financial planning can be done in a number of ways, some live off passive income, social security (Check out how to get a copy of my social security card), or pensions, while many others choose to safely draw down their assets. Other folks augment their income with part-time work, some folks side hustle, or some go into “mini-retirements” which involve periods of short full-time employment. These are all fine options and to each his own path that suits his or her comforts. I’m not particularly critical about what qualifies as “retirement” and what does not. In my mind, leaving the 9-5, 5-a-week plan for any other alternative is a pretty good objective–no need to criticize if somebody chooses a varied alternative to your retirement plan. Many don’t have the opportunity to retire at an early age, most people retire around 50-60 years old.

For Retire29, my goal is to exit the traditional workforce on/around September 3rd, 2019—just over four years from now. From that point on, I’ll fund my lifestyle 100% by using dividends, interest, and rental income, once I retire I’ll put in place my living trust and decide how to handle all my assets (click here for more info). I’ll continue to generate some small side hustle income for a few years that will serve to add to the pile, pay down our mortgage principal, and meet any unknowns that may arise. I know I’d be paranoid if I had to draw down investment principal to fund my lifestyle. Living off of an ever-increasing stream of passive income (via dividend and rent increases) and shunning investment principal drawdown is certainly the way for me and fits my psychology.

I also expect to always make some money, because I enjoy adding value and content to the financial netspace, and I will always love following and writing about the stock market. This side hustle income will not be necessary, but having that margin of safety and the ability to add to principal will be reassuring at the outset.

This is the full roadmap:

Today’s Snapshot

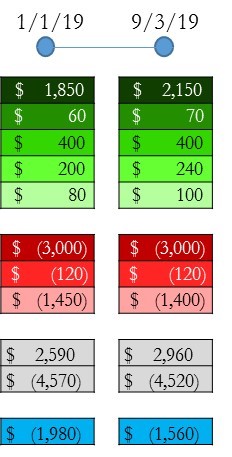

I have about $830 of non-job income in an average month. About $60 of this is from side hustles that I would continue to do even after I quit the traditional workforce, while the rest is from dividends and interest.

Compare this to $5,500 in expenses (I’m using some averages here based on recent financial reports and current expenses), and you’ll see I’m still quite far away from early retirement with a deficit of -$4,670/mo. However, I have a reasonable plan for increasing the green numbers and decreasing the red numbers, and I’m going to discuss the roadmap below by looking at checkpoints and the steps I’ll be taking between each point.

Today – January 1st, 2016

Income: I originally wanted to get to $1,000 in average dividends by the end of this year. That is looking quite unlikely. I could move my huge non-dividend technology allocation of my portfolio to dividend paying stocks, but I think long-term capital growth is more important at this stage, and I expect that the total return will be better in these non-dividend stocks.

Although, a more reasonable $850 by year end (a $120/increase from today) is essentially assured. IRA/401k contributions will amount to an extra $35/mo, another $20/mo for reinvested dividends, another $35/mo for dividend increases, and another $30/mo for contributions to my taxable brokerage bond funds.

There is upside potential here, covered calls will generate a few extra dollars, and the potential exists for Google to initiate a dividend this year with their new CFO and the beckoning for one from the street. I’m also not accounting for any side hustle contributions to the dividend accounts.

I’ve made an average of $70/mo in the five months of writing on SeekingAlpha. I think I can do better, so $100/mo by the end of the year is a reasonable goal with a bit of effort.

The website crossed $10/mo of revenue in May ’15, and this month is tracking for even higher. Averaging $10/mo in revenue was my goal for 2015–so it looks like I’ll be exceeding that. This is obviously really small ball, but slow and steady progress is good to see at this stage in the game.

Expenses: No big changes to housing expenses. But, for transport, the plan is to sell the Corvette once the loan is satisfied, which will be late this summer. Even if I don’t sell the ‘Vette by then, though, the Mercedes will be fully paid by January, anyway. The payments are $400 and $300/mo, respectively, so we’ll be seeing reductions in car payments no matter what happens. I only decreased my plan to $600/mo. rather than $200 (if both cars are paid), because we may choose to finance our follow-on “family friendly” vehicle. Most bloggers abhor car loans, but if you can get a good price and can finance at 2%, then why not?

I expect other expenses to continue a slight downward trend. We are getting better at credit card hacking, so travel expenses are becoming less and less. We’re also using gift cards more, have made countless energy-saving upgrades to our home, are cooking more meals at home, and I am doing some bike commuting. I think dropping another $100 in average monthly “other” expenses is a safe bet.

January 1st, 2016 – January 1st, 2017

Income: I’ve been talking about it a long time, but next year it will have to happen. Fellow blogger FI Fighter is probably the greatest example I’ve seen regarding the ability of rental properties to vastly increase net worth and passive income. I will seek to find a rental property next year that yields $150/mo after expenses. I’ll also continue to increase my readership on SeekingAlpha and the blog, which will generate some incremental income via page views and Adsense.

Every time I run the numbers, achieving 32% growth in dividend income next calendar year seems more and more possible. This increase of $275/mo in dividends will come from the following:

Expenses: More important than income, though, is continuing expense reductions. Next year I’ll certainly close out both car loans and sales (assuming I can’t this year, although I expect that I will). With that will almost certainly come a reduction in insurance, gas and taxes. I’ll also continue to optimize spending in other areas of our lives like energy efficiency, maximizing credit card rewards and cash back, and doing more bicycle commuting. I’d like to knock $100 off our monthly expenses through some of this fat-trimming.

January 1st, 2017 – September 3rd, 2019

January 1st, 2017 – September 3rd, 2019

{kind=link}

Income: The following 2.75 years will be much of the same–keep taxes low by maximizing 401(k) and IRAs, keep savings high, make more money at work, and work to continue side hustles. My calculations show that I can increase dividend income by about 27% per year. Now, that sounds pretty aggressive, but it’s actually not so crazy when if you’re working off of a relatively small investment base. Why 27%? 8% dividend increases, 4% reinvestment of yield, 2% covered calls, 10-15% new capital contributions. During this period, I’ll target a second entry-level rental property in our current area, and attempt to increase our total monthly rental cash flow to $400/mo.

I think that by the autumn of 2019, I could conceivably get this website to generate ~$100/mo in revenue, and that I could write 2-3 SeekingAlpha articles per month (~$240).

Expenses: Not much change here, other than we’ll be trying to continue optimization of our expenses outside of housing costs. I still see so much opportunity for expense reduction in our monthly statements–most obviously in other/household costs and food. I’m not talking life changing amounts of expense reduction here, just working on the edges and maintaining a frugal mindset when purchasing anything. At each point-of-sale, ask if it can be purchased elsewhere for cheaper, if we can do without it completely, and seek to utilize cash back cards, gift cards, Amazon, credit card hacking, and Craigslist rather than paying retail.

As long as you’re familiar with bicycle laws in new york, bicycling can be a great way to get around Manhattan. Transportation will fall to the baseline level of $120, as we will not have any legacy car payments, I will continue commuting via bike, so our total expenses will be just personal property taxes, 1-2 tanks of gas per month, minor maintenance, and liability insurance, which I figure to be $100-120/mo. in total.

September 3rd, 2019 – Retirement

September 3rd, 2019 – Retirement

Beginning on September 3rd, 2019, I’ll start retirement preparations. I will continue working during this time, but the “two-weeks notice” date will become imminent. There will be several big changes occurring in our household during this preparatory period:

1. Upon the last day in the workforce, I will move my 401(k) into dividend growth stocks. Along with some minor continuation of normal passive income growth, this will cause my dividend growth to exhibit a step increase.

2. Upon retirement, or shortly before, I will begin to transition to a part-time writer mentality and schedule, committing some time each day or with some recurrence to freelance financial writing. This is what causes the step increase in writing income.

3. This is the big one and the biggest change from my original big goal roadmap. We will sell our primary home in NoVA to a house buyer like the House Buyers of America and use the equity to make a substantial (50-60% of home value) down payment on a similar house in a far lower cost-of-living locale such as Florida, Colorado, North Carolina or Georgia. We’ve identified great locations that suit early retirement based on many factors in this post, and is worth a read.

After careful consideration, the numbers simply didn’t add up for the cost and mental toll that managing a distant, and expensive property would entail. We originally thought we could refinance and rent out our primary home. However, our total expenses for this house (post-refi) would be somewhere around $2600/mo (of which about $600 would be principal paydown). Our net revenue from the property would be about $2200/mo ($2,700 rent – $270/mgmt fee – $230/vacancy allowance). We would be cash-flow negative each month, although our net worth would increase slightly. This sounds too hard, and the numbers bear that out. Following the 1% rule of rental efficacy (the monthly rent should be 1% of the home value in order for a rental to make sense), this house just doesn’t qualify (not even close). Our rent-to-value ratio would be more along the 0.5% route, so we’re way off.

If we do get two other rental properties in our current area, they will be cash flow positive even with a manager, otherwise we won’t get involved (plus the home values and payments will be much lower).

The upside to this decision to sell our home and put it toward our retirement home is that our housing payments in retirement will be much lower than previously thought. $700/mo, even after accounting for taxes, would be the norm. What’s more, we could get that mortgage (somewhere between $60-80k) paid off in just four or five years if we put our side hustle income toward it.

What Could Go Right? What Could Go Wrong?

There are many things that could impact this plan for the better or worse:

Things that Could Help the Plan

- The market sells off considerably, allowing new investment contributions and reinvested dividends to generate more income

- A company that currently pays no dividends to me (e.g. Google, Tesla, Netflix, Bank of Internet), decides to initiate a dividend

- I receive raises and/or promotions at work, allowing me more money to throw at passive income generation

- I strengthen my side hustle muscle, and find ways to generate more income outside of the office.

- We rent out our basement in our current home, which would generate significant income that would go straight to passive income creation.

Things that Could Hurt the Plan

- I addressed a number of high visibility things that are often touted as things that could kill this plan, like health insurance, costs of college, costs of raising kids, and the fact that most of my money will be in tax-deferred accounts. However, I addressed these concerns and don’t see them as issues, in this post.

- The market continues to skyrocket for years to come. This means new capital and reinvested dividends generate less passive income.

- Dividends are cut. This is unlikely to happen in most of the companies I own, as most have paid increasing dividends for years (even through 2008-9), however, for some riskier companies, this is possible.

- I’m unable, for whatever reason, including self-inflicted reasons, to generate rental income.

- I don’t follow through on expense reduction nor do I follow through on side hustling to the degree I need to.

In Conclusion

That’s the plan! I would really, really (I mean it 🙂 ) appreciate your thoughts and comments below, as I know I haven’t thought of everything. Where am I crazy, what doesn’t make sense, does something look impossible?

In the end, I need to remind everyone that I understand that this is an aggressive plan, and that, in the end, the only plan that matters is God’s. However, a plan of any kind is important to have, and even if I fail at perfectly executing the above, a slight failure is still going to result in a very early retirement.

Looking forward to your thoughts!

Eric

One risk would be in the value of your home equity 4 years from now. What if interest rates go up the next 4 years and housing prices decrease a decent amount. You may have less equity than expected, and sure, cheap houses in Florida went down by the same percentage also, but on a much smaller initial amount. I don’t recall the detailed plan to address this, but another concern would be having enough dividend income outside of retirement accounts. Overall it sounds pretty doable. It’s really more of a question of how low can your expenses go, and how content are you having a lot of free time to fill with those limited expenses. The risk of having unlimited “vacation days” but your budget is so tight that it’s difficult to travel, short of camping wherever you go. Getting a more tangible idea of how you would plan your free time would be a good thing to do. Then you can better estimate what the true expenses might be.

dh,

Thanks for commenting. You make some valid points, and it details the unknowns involved with planning out an aggressive timeline for than a year into the future. To address your points individually:

1. Home price decreases: Interest rates have really just one direction to go, if you assume that home prices will move inversely to interest rates (which is a reasonable assumption), then home prices may definitely decline. On the one hand, this will lead to less equity in our current home, meaning a smaller down payment on our retirement home–which will lead to larger payments at the outset of retirement. One the other hand, this knife cuts both ways. If home prices are declining, then a fair bet is that our retirement home price would also decline–perhaps not be the same amount, but some, nonetheless. The point is clear, though, the housing costs I’m projecting may be a hundred or two off, because in all cases, the mortgage balance will be much, much lower, and the impact of interest rates will be significantly diminished.

2. Retirement account lock-ups: I talked about this in more detail in this post, and do not see this as much of an issue. I will be able to withdraw, penalty free, contributions to Roth IRAs that have been there for over five years–which will be enough for several years of expenses. Factor in that a good bit of dividend income will be from “free and clear” accounts and side hustle income, and we will have more than enough coverage for the first few years. Each year of retirement, we will also move ~$30k from Traditional IRAs to Roth IRAs. We will pay taxes on this, but given our standard deduction and exemptions, the tax bill will be roughly zero. We can then withdraw those transfers from our Roth five years later (starting in 2024, approximately).

3. Travel: We’ve only been credit card hacking for three months or so, and we already have over ten hotel nights available and enough Southwest miles to fly four to seven round trips (depending on distance). And, we’re accruing more every couple months. In a way, camping would probably be the most expensive way for us to travel, given the free flights and nights available to us. The savings and potential is real. Visit ThePointsGuy, he’s an amazing blogger who covers this better than anyone.

4. Free Time: I posted about my Retirementality, and the abundance of things I’d love to do in my new lifestyle. Work is always available to me.

5. Expenses Are So Low: I’ll admit, the expense amount is pretty low and quite aggressive. I’m not certain we can get there and still live an ideal lifestyle. I think it’s possible, but I’ll admit it’s an unknown. To our credit, though, is that I’ve built in an over $1,000 buffer/surplus, so we aren’t looking at a hard and fast expense threshold. What’s more, is that dividend income will grow each year as companies raise dividends, and any excess income I still generate will just get thrown on the pile. And, worst case scenario, if things don’t work out as planned, I can always stay in the workforce for a few extra months or a year, work part-time, or (worst case scenario) go back to working full time for a short stint later on in retirement. It’s life, it’s very flexible.

Thanks much for commenting and would love to hear your follow-up.

Eric

I like how you mapped it out for every year! Great idea! It seems like you have really thought out alternatives! I have a crazy excel spreadsheet that I use, recently I added in extra costs for my kids when they are teenagers for sports and extra clothes, field trips and extra food! Kids and healthcare seem to be my biggest variables for our planning.

Hi Mrs SSC,

Yah, I’ve been there–a lot of excel went into all of this. I have to make something a bit prettier and permanent, though, for me to have something to measure against.

I may have to make some adjustments for kids and for healthcare, although I don’t think they’ll be drastic. Kids so far for us have been cheap, and health care is made easy for early retirees tanks to the ACA. However, that’s why I’ll have to readjust every year. Thanks so much for commenting!

Eric

I like how you have put a lot of thought into this. 2019 seems really close! I am aiming for 2025 but doing what I can to bring that number closer. Part of our strategy is to downsize the house and I worry about the housing market like the commenter above mentioned. Our house will probably drop by a greater percentage than a smaller one but we will play it by ear. Husband is really interested in income properties but I just can’t go there. Good luck – will be watching with interest.

Hey May,

Yah, there are certainly some unknowns as it relates to housing. But, no matter what transpires with the housing market, the effect will be minimal on the retirement date. In any scenario, our housing costs will be drastically reduced with moving to a lower cost of living location.

We haven’t ventured into income properties quite yet, so not sure how that will work out when we cross that bridge next year. Four years still seems like an eternity!

Thanks so much for tuning in.

Eric

This looks like a great plan to start with. As always, flexibility will be key to survive.

One element that fascinates me is the covered call writing. You plan to make 2pct per year off that. Can you detail this a little? It is a strategy I started this month, I am am curious to see how others are doing.

cheers

Hello Amber Tree,

I would be happy to expound on covered call writing. In fact, I already have! I hope you enjoy that article as well. 2% is certainly a rough estimate, I’ve made about 0.8% this past four months–so I think that’s a reasonable amount to estimate going forward.

Thanks so much for commenting!

Dividend Mantra’s implosion brought me here. Reminds me of Dividend Mantra site, but somewhat less person as you are not disclosing all your income (totally understandable). As for your plan, if I am understanding this right, you plan on living off of a net + $1200/month in retirement plus so side income starting in 2019? Do you plan on joining the Amish? That’s a pretty small number for a single guy…much less for a guy with a wife (who does not work) and at least 2 kids. What am I missing here? I am 35, US Navy (11 years, Officer), wife (who works) and 1 kid. We’re approaching 3/4 of a million dollars in savings and we still don’t feel comfortable retiring until I reach military retirement in 2025. I just think you are underestimating the expenses life can bring, especially while raising kids. Good luck to you though.

Hi Christian,

Glad you found your way here, even if no under great circumstances. I followed Jason’s journey (he stops by here once in a while, too), and it really was something watching his site fall apart so quickly.

I plan on living off of about $2,200-$2,400 per month starting sometime mid-2020. The elimination of the mortgage (via selling our big DC home and moving to Florida or somewhere cheaper and buying outright), goes a long way in achieving this spending goal.

The portfolio value needed to support that level of monthly income will be around three-quarters of a million, give or take. I cover both the detailed expense breakout and the portfolio needed in this post, and I think you might really enjoy it!

I’ve seen other bloggers with absolutely ridiculous expense goals that are wholly separate from reality, and when I read that I immediately tune them out as unreasonable. I’d hate to lose a reader early on for that reason. Thanks so much!

Eric